Why You Need an Acquirer to Process Payments

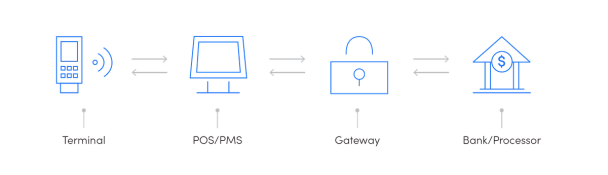

When you accept a credit card payment, there are many components that work together to process this transaction. Shift4’s end-to-end payment solution is unique in that it handles all of these steps behind the scenes to deliver a seamless commerce experience. One component involved in this process is the role of acquiring bank.

The acquirer — also known as a credit card bank, acquiring bank, or merchant bank — is a bank or financial institution licensed as a member of a card association (such as Visa or Mastercard) and is responsible for opening and maintaining the merchant’s bank account. The acquirer can also act as a settlement bank, facilitating merchant payment communication and settlement.

What Is the Role of the Acquirer in the Payment Process?

Even though transactions only take a few seconds, there is a lot going on under the hood before the purchase is complete. First, the card information is encrypted by the payment gateway and is then sent for approval. The acquirer’s job comes toward the end of this process. They authorize or reject card transactions as they come in and connect to the issuing bank on the merchant’s behalf during the payment process. Once a transaction is approved, the funds are transferred to the merchant’s account.

After getting the card information from the payment gateway, an acquirer is responsible for the following:

- Authorization: Asking the issuer whether the card is valid and whether there are sufficient funds in the account to complete the transaction.

- Authentication: A voluntary verification of the cardholder’s identity after entering the card details during purchase. Typically, 3D Secure is used for authentication.

Your choice of acquirer should be guided by their support for your business model. Additional factors to consider include the following:

- The types of cards the acquirer supports: Ensure that they have all the card networks you accept in their portfolio. Also, ask for other payment methods if you need them.

- (For international businesses) Locations and currencies the acquirer supports: Does the list include the country in which your company is registered? Check that the acquirer approves any and all currencies you intend to accept on your website.

- The average transaction amount: This will help you calculate how much you’ll be charged for each transaction. Note that an acquirer may charge a merchant various fees, which will be specified in their agreement. Fees are charged to cover the costs associated with network processing and merchant account-related services.

- The average number of transactions: Speaking of pricing, double-check the rates to ensure that you won’t have to pay extra monthly fees, which can be costly, especially in the early stages. Furthermore, you can negotiate rates if you own a company that handles numerous daily transactions.

- Responsive support: You need to be assured that any payment issue will be quickly addressed.

- Recurring payments: If you’d like to offer subscriptions, your acquirer needs to support recurring payments.

Simplifying the Process with End-to-End Payments

As you can see, merchants have to navigate overwhelming complexity before they can accept a single payment. Fortunately, Shift4 offers a unique end-to-end payment solution that delivers all the connections to the entire transaction process. This simplified approach has numerous benefits, including lower total cost, faster implementation, streamlined support, and much more. Our all-in-one ecosystem includes:

- Secure payment gateway with tokenization and PCI-validated point-to-point encryption

- P2PE-enabled EMV devices with lifetime free replacements

- 500+ POS, PMS, and ecommerce integrations

- Processor connection

- Future-proof updates with the latest technologies and trends

- 24/7 customer support for all your payments needs

Want to learn more? Contact us today at sales@shift4.com or at 888.276.2108.